Mortgage Loan Basics for New Borrowers

January 5, 2022

If you are new to being a house hunter, there are good things to know about mortgages going into the process. It doesn’t matter if you seek an FHA home loan, a conventional mortgage, or any other option; some mortgage issues will potentially affect your transaction no matter which option you decide on.

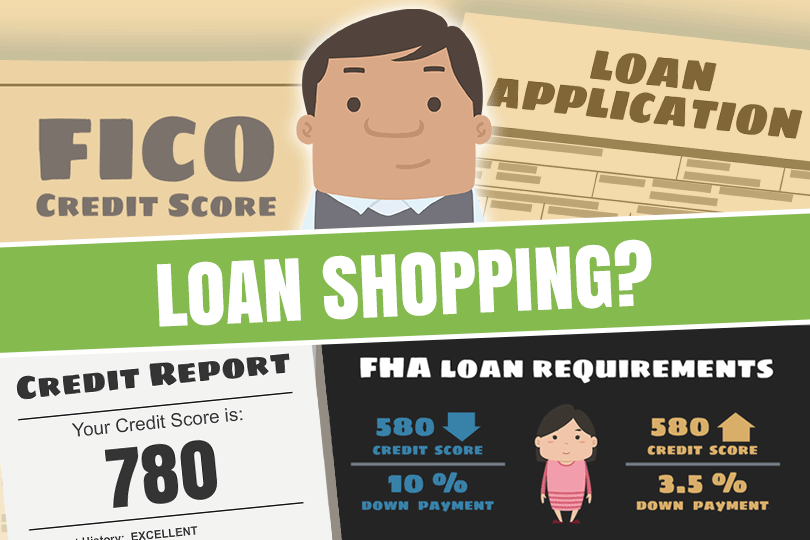

One such issue? Down payments. An FHA loan down payment, for example, must be paid independently of any other closing costs. You can’t pay $400 for an appraisal (this number is for example purposes only, your experience may vary) and expect to have that $400 subtracted from the amount of the down payment.

Another thing to remember about down payments is that no matter where your down payment money comes from (a grant, a gift from a family member, from your own savings, etc.) your lender will require you to document the source of the money.

That means being able to show where specifically the funds came from and that they do not come from payday loans, cash advances on a credit card, or any other unapproved source.

Another area to think about as a new borrower? Your plans for the mortgage. Do you think you might sell or refinance the home at some point? If so you will want to ensure the purchase agreement you sign does not include a penalty for the early payoff of the loan amount.

Conventional mortgages may well feature such a penalty and you will want to ask upfront if that is going to be in your loan contract. FHA mortgages actually forbid the prepayment penalty which is one reason to consider an FHA loan as one of your options.

The prepayment penalty when present may affect how you pay your loan over time (larger payments each month, for example, will result in early payoff) or whether or not to refinance your home.

You should also ask the lender (if you decide to go with a conventional mortgage) how much the prepayment penalty might be and how it must be paid--there may be a special procedure required for submitting the penalty, the final mortgage payment, or both.

The nature of your home loan is also an important factor. You can apply for a conforming loan that is at or below the local loan limit for your county, or you could apply for a non-conforming loan that exceeds the area limit.

Non-conforming loans are possible for FHA mortgages as well as conventional loans but be advised that non-conforming loans / jumbo loans may cost more and have higher credit requirements.

At some point, no matter what kind of mortgage loan you get, you may wish to consider refinancing your mortgage. It is a good idea to learn what options are available to you depending on what kind of loan you took out originally. For example, FHA mortgages have the option to be refinanced using an FHA Streamline Refinance loan which uses your original application data and has no FHA-required appraisal or credit check. FHA Streamlines are only for existing FHA loans and may result in a lower monthly payment, a lower interest rate, or some other tangible benefit to the borrower.

------------------------------

RELATED VIDEOS:

Here's the Scoop on Conventional Loans

When Do You Need a Cosigner?

Analyzing Your Debt Ratio

One such issue? Down payments. An FHA loan down payment, for example, must be paid independently of any other closing costs. You can’t pay $400 for an appraisal (this number is for example purposes only, your experience may vary) and expect to have that $400 subtracted from the amount of the down payment.

Another thing to remember about down payments is that no matter where your down payment money comes from (a grant, a gift from a family member, from your own savings, etc.) your lender will require you to document the source of the money.

That means being able to show where specifically the funds came from and that they do not come from payday loans, cash advances on a credit card, or any other unapproved source.

Another area to think about as a new borrower? Your plans for the mortgage. Do you think you might sell or refinance the home at some point? If so you will want to ensure the purchase agreement you sign does not include a penalty for the early payoff of the loan amount.

Conventional mortgages may well feature such a penalty and you will want to ask upfront if that is going to be in your loan contract. FHA mortgages actually forbid the prepayment penalty which is one reason to consider an FHA loan as one of your options.

The prepayment penalty when present may affect how you pay your loan over time (larger payments each month, for example, will result in early payoff) or whether or not to refinance your home.

You should also ask the lender (if you decide to go with a conventional mortgage) how much the prepayment penalty might be and how it must be paid--there may be a special procedure required for submitting the penalty, the final mortgage payment, or both.

The nature of your home loan is also an important factor. You can apply for a conforming loan that is at or below the local loan limit for your county, or you could apply for a non-conforming loan that exceeds the area limit.

Non-conforming loans are possible for FHA mortgages as well as conventional loans but be advised that non-conforming loans / jumbo loans may cost more and have higher credit requirements.

At some point, no matter what kind of mortgage loan you get, you may wish to consider refinancing your mortgage. It is a good idea to learn what options are available to you depending on what kind of loan you took out originally. For example, FHA mortgages have the option to be refinanced using an FHA Streamline Refinance loan which uses your original application data and has no FHA-required appraisal or credit check. FHA Streamlines are only for existing FHA loans and may result in a lower monthly payment, a lower interest rate, or some other tangible benefit to the borrower.

------------------------------

RELATED VIDEOS:

Here's the Scoop on Conventional Loans

When Do You Need a Cosigner?

Analyzing Your Debt Ratio

Do you know what's on your credit report?

Learn what your score means.