Buying Your First Home with an FHA Loan

June 3, 2023

If you’re thinking about buying a home this year and you need to save more money upfront on your down payment, an FHA mortgage is an option to consider thanks to its minimum 3.5% down payment. There are other perks to FHA loans, as we’ll discover below:

No Early Payoff Penalties on FHA Mortgages or Refinance Loans

FHA loan rules don’t allow the lender to charge a penalty for paying off your loan early, whether that means paying extra on your mortgage payment every month, refinancing the loan, or selling the house.

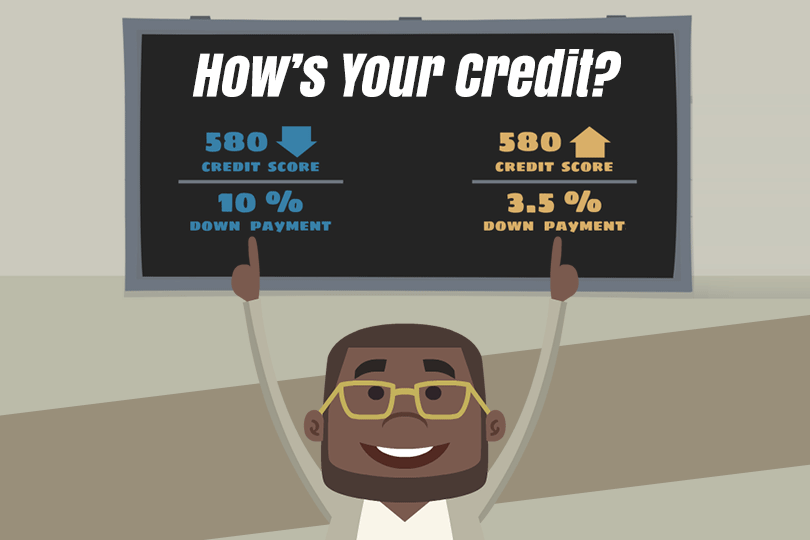

FHA loans require a minimum FICO score of 580 or higher for the lowest down payment.

FHA mortgage loan rules in HUD 4000.1 state that a borrower should have two years of employment history, though you don’t have to have that history with just one employer.

Mortgage Loan Interest Rate Issues

Your FICO scores play an important role for the lender when it’s time to offer a mortgage loan interest rate.

The lower your rate, the more you save over the lifetime of the mortgage. Some FHA borrowers choose a fixed-rate mortgage because they want to keep the home for a long time.

But when interest rates are high, an FHA adjustable-rate mortgage can help; these loans have a lower introductory rate; adjustable-rate mortgages are best for borrowers who make a plan to deal with the interest rate adjustments once they start. It’s best to sell, refinance, or pay more each month on your mortgage once those rate changes begin.

------------------------------

RELATED VIDEOS:

What You Need to Know About the Appraisal Fee

The Appraisal is an Important Requirement

Build Your Dream Home With a One-Time Close Loan

No Early Payoff Penalties on FHA Mortgages or Refinance Loans

FHA loan rules don’t allow the lender to charge a penalty for paying off your loan early, whether that means paying extra on your mortgage payment every month, refinancing the loan, or selling the house.

- The lender can’t penalize you for paying your mortgage off ahead of schedule or making extra payments.

- Some borrowers split their mortgage payment in half and pay once every two weeks, which adds an extra mortgage payment per year.

FHA loans require a minimum FICO score of 580 or higher for the lowest down payment.

- If your FICO scores are between 500 and 579, FHA loan rules say you must pay 10% down.

- Lender standards will also apply, so make sure you ask what those additional standards might be.

- Typical lenders may require FICO scores in the 600 range.

FHA mortgage loan rules in HUD 4000.1 state that a borrower should have two years of employment history, though you don’t have to have that history with just one employer.

- Frequent job changes may be an initial concern, but they may be acceptable to FHA lenders if you have been upwardly mobile during those job changes.

- Your employment record will be reviewed and if you have concerns about that history, consider explaining (in writing) any circumstances that might need more clarification.

- FHA loan rules have certain flexible income guidelines intended for seasonal workers, people earning commissions, self-employed applicants, and freelance/contractors to qualify for a home loan.

Mortgage Loan Interest Rate Issues

Your FICO scores play an important role for the lender when it’s time to offer a mortgage loan interest rate.

The lower your rate, the more you save over the lifetime of the mortgage. Some FHA borrowers choose a fixed-rate mortgage because they want to keep the home for a long time.

But when interest rates are high, an FHA adjustable-rate mortgage can help; these loans have a lower introductory rate; adjustable-rate mortgages are best for borrowers who make a plan to deal with the interest rate adjustments once they start. It’s best to sell, refinance, or pay more each month on your mortgage once those rate changes begin.

------------------------------

RELATED VIDEOS:

What You Need to Know About the Appraisal Fee

The Appraisal is an Important Requirement

Build Your Dream Home With a One-Time Close Loan

Do you know what's on your credit report?

Learn what your score means.