FHA Loans: When the Appraisal Comes in Low

January 31, 2022

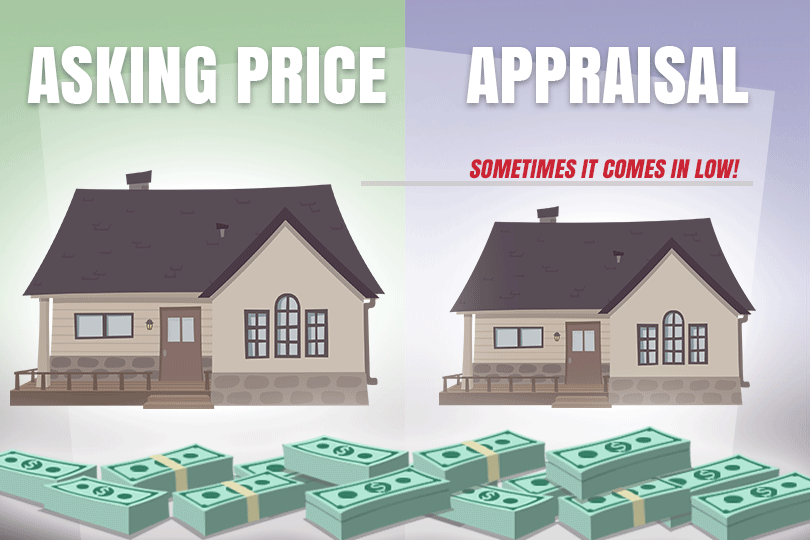

What happens when you apply for a home loan, but the appraisal on the property comes in lower than the asking price? Most government-backed mortgages feature a portion of their loan underwriting rules that includes the ability to walk away from such a situation without penalty.

For some government-backed home loans, it’s known as an “escape clause”. For first-time homebuyers applying for an FHA mortgage, this option is a very important one since under those circumstances you are still allowed to buy the home but with some caveats.

HUD 4000.1 (the FHA Single-Family Home Lender’s Handbook) provides guidance for participating lenders that requires a legally-binding clause to be inserted into any commitment to purchase the home. The clause guarantees that the borrower does not forfeit earnest money or retain an obligation to purchase the property if the appraisal comes back lower than the sale price.

The escape clause may read something like this, or exactly like this:

“It is expressly agreed that notwithstanding any other provisions of this contract, the purchaser shall not be obligated to complete the purchase of the property described herein or to incur any penalty by forfeiture of earnest money deposits or otherwise, unless the purchaser has been given, in accordance with HUD/FHA or VA requirements, a written statement by the Federal Housing Commissioner, Department of Veterans Affairs, or a Direct Endorsement lender setting forth the appraised value of the property of not less than $___________*.”

The “template” for that clause above is found in HUD 4000.1. The clause contains wording that the borrower has the option to proceed with the loan “…without regard to the amount of the appraised valuation.”

And just as important as the “escape clause” itself? The understanding that no matter what the borrower chooses to do, the appraisal is not a guarantee from the FHA or HUD.

“The appraised valuation is arrived at to determine the maximum mortgage the Department of Housing and Urban Development will insure. HUD does not warrant the value or condition of the property. The purchaser should satisfy himself/herself that the price and condition of the property are acceptable.”

Borrowers are, thanks to the escape clause, free to refuse an FHA loan transaction where the appraisal comes in at a value lower than the sale price. This is allowed in part because otherwise the buyer is forced to pay the difference out of pocket--that sum cannot be rolled into the loan.

If you aren’t sure how this will affect your home loan transaction, ask your loan officer to explain how these rules may affect your transaction and how to proceed if those rules are applicable to you. Be sure to ask if there are any rules that apply in terms of how long you have to make up your mind, what is required should you decide to walk away, and how much you are expected to pay at closing time if you choose to proceed with the loan anyway.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

For some government-backed home loans, it’s known as an “escape clause”. For first-time homebuyers applying for an FHA mortgage, this option is a very important one since under those circumstances you are still allowed to buy the home but with some caveats.

HUD 4000.1 (the FHA Single-Family Home Lender’s Handbook) provides guidance for participating lenders that requires a legally-binding clause to be inserted into any commitment to purchase the home. The clause guarantees that the borrower does not forfeit earnest money or retain an obligation to purchase the property if the appraisal comes back lower than the sale price.

The escape clause may read something like this, or exactly like this:

“It is expressly agreed that notwithstanding any other provisions of this contract, the purchaser shall not be obligated to complete the purchase of the property described herein or to incur any penalty by forfeiture of earnest money deposits or otherwise, unless the purchaser has been given, in accordance with HUD/FHA or VA requirements, a written statement by the Federal Housing Commissioner, Department of Veterans Affairs, or a Direct Endorsement lender setting forth the appraised value of the property of not less than $___________*.”

The “template” for that clause above is found in HUD 4000.1. The clause contains wording that the borrower has the option to proceed with the loan “…without regard to the amount of the appraised valuation.”

And just as important as the “escape clause” itself? The understanding that no matter what the borrower chooses to do, the appraisal is not a guarantee from the FHA or HUD.

“The appraised valuation is arrived at to determine the maximum mortgage the Department of Housing and Urban Development will insure. HUD does not warrant the value or condition of the property. The purchaser should satisfy himself/herself that the price and condition of the property are acceptable.”

Borrowers are, thanks to the escape clause, free to refuse an FHA loan transaction where the appraisal comes in at a value lower than the sale price. This is allowed in part because otherwise the buyer is forced to pay the difference out of pocket--that sum cannot be rolled into the loan.

If you aren’t sure how this will affect your home loan transaction, ask your loan officer to explain how these rules may affect your transaction and how to proceed if those rules are applicable to you. Be sure to ask if there are any rules that apply in terms of how long you have to make up your mind, what is required should you decide to walk away, and how much you are expected to pay at closing time if you choose to proceed with the loan anyway.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

Do you know what's on your credit report?

Learn what your score means.