FHA Loan Requirements in 2021 and Beyond: Credit And Income

July 26, 2021

What are the credit and income requirements for FHA loans in 2021 and beyond? There is still time to take advantage of the higher mortgage loan limits for FHA home loans this year, and if you don’t know what it takes to be approved for an FHA single family loan this year, keep reading.

FHA Loan Credit Requirements

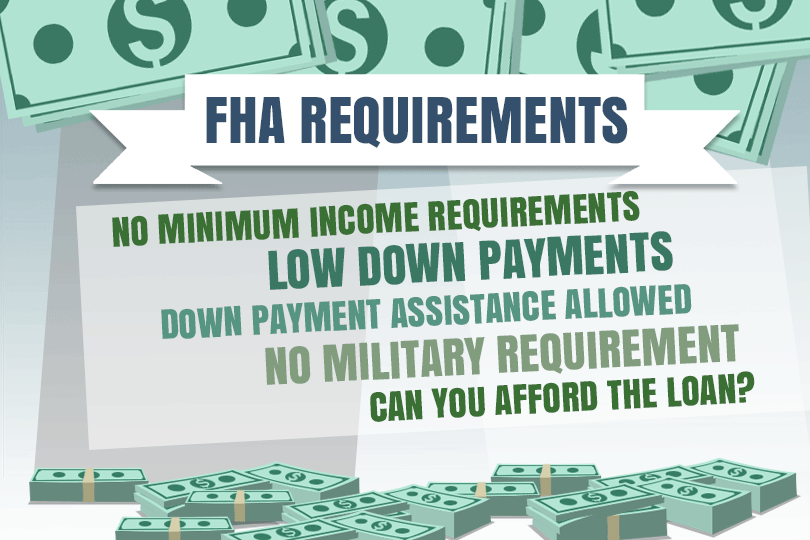

The most important thing you should know as a buyer about FHA loan credit requirements this year is that FHA standards (580 or better FICO scores for the lowest down payment) are not the only minimum credit score standards at work--the lender’s own standards also count.

That means you will want to start monitoring your credit and maintaining a record of 100% on-time payments on all financial obligations at least a year ahead of your application.

That’s not something many people want to hear, because it can be challenging to make those payments on time, every time. But if you want to own your own home, that is what it takes.

Pro Tip: The three most important things you need to do to improve your credit are the previously mentioned 100% on-time payment rate, plus a lower debt-to-income ratio (try to get yours down below 43% of outgoing total monthly debt compared to monthly income) and lower your credit card balances to well under half your credit limit on each card.

FHA Loan Income Requirements

The good news about FHA mortgages is that there is no minimum income amount you need to qualify. It’s more important that you be able to actually afford the loan with your current income compared to your existing debt. The debt ratio or DTI you carry will affect the loan approval process.

That means that your current income should be sufficient to meet payment requirements for both your current bills AND your new mortgage loan.

FHA loan guidelines instruct the lender to determine this based on your monthly debt payments but keep in mind that certain debt (such as medical debt) may be excluded depending on circumstances.

Try using an online mortgage calculator to help determine whether your loan amount is something you can afford. Even with down payment assistance, some borrowers may find they need to make adjustments in their budget to afford the expense of the new loan. Giving yourself more planning time ahead of your loan application is a good idea. Know what you are getting into before you commit.

Pro Tip: Your lender won’t just look at your income. The lender also looks at how long you have been earning that income, which can be critical for those who have switched from one type of earning to another--from salary to commission, from being an employee to being a contractor, etc.

If you have recently changed how you earn your money, be sure to ask the lender how long you need to earn that new type of income before it may be counted as part of your verifiable income. Even first-time home buyers should expect this to be a crucial factor in buying single-family homes.

Remember, the stronger your credit and income are in the eyes of the lender, the closer you get to home loan approval. FHA loan requirements in 2021 are not too high to qualify, but it may take some work for some borrowers to get truly ready for their loan application. It is also important for those who have a bankruptcy in their credit history to wait until their bankruptcy has been discharged to pursue a new home loan in many cases.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

FHA Loan Credit Requirements

The most important thing you should know as a buyer about FHA loan credit requirements this year is that FHA standards (580 or better FICO scores for the lowest down payment) are not the only minimum credit score standards at work--the lender’s own standards also count.

That means you will want to start monitoring your credit and maintaining a record of 100% on-time payments on all financial obligations at least a year ahead of your application.

That’s not something many people want to hear, because it can be challenging to make those payments on time, every time. But if you want to own your own home, that is what it takes.

Pro Tip: The three most important things you need to do to improve your credit are the previously mentioned 100% on-time payment rate, plus a lower debt-to-income ratio (try to get yours down below 43% of outgoing total monthly debt compared to monthly income) and lower your credit card balances to well under half your credit limit on each card.

FHA Loan Income Requirements

The good news about FHA mortgages is that there is no minimum income amount you need to qualify. It’s more important that you be able to actually afford the loan with your current income compared to your existing debt. The debt ratio or DTI you carry will affect the loan approval process.

That means that your current income should be sufficient to meet payment requirements for both your current bills AND your new mortgage loan.

FHA loan guidelines instruct the lender to determine this based on your monthly debt payments but keep in mind that certain debt (such as medical debt) may be excluded depending on circumstances.

Try using an online mortgage calculator to help determine whether your loan amount is something you can afford. Even with down payment assistance, some borrowers may find they need to make adjustments in their budget to afford the expense of the new loan. Giving yourself more planning time ahead of your loan application is a good idea. Know what you are getting into before you commit.

Pro Tip: Your lender won’t just look at your income. The lender also looks at how long you have been earning that income, which can be critical for those who have switched from one type of earning to another--from salary to commission, from being an employee to being a contractor, etc.

If you have recently changed how you earn your money, be sure to ask the lender how long you need to earn that new type of income before it may be counted as part of your verifiable income. Even first-time home buyers should expect this to be a crucial factor in buying single-family homes.

Remember, the stronger your credit and income are in the eyes of the lender, the closer you get to home loan approval. FHA loan requirements in 2021 are not too high to qualify, but it may take some work for some borrowers to get truly ready for their loan application. It is also important for those who have a bankruptcy in their credit history to wait until their bankruptcy has been discharged to pursue a new home loan in many cases.

------------------------------

Learn About the Path to Homeownership

Take the guesswork out of buying and owning a home. Once you know where you want to go, we'll get you there in 9 steps.

Step 1: How Much Can You Afford?

Step 2: Know Your Homebuyer Rights

Step 3: Basic Mortgage Terminology

Step 4: Shopping for a Mortgage

Step 5: Shopping for Your Home

Step 6: Making an Offer to the Seller

Step 7: Getting a Home Inspection

Step 8: Homeowner's Insurance

Step 9: What to Expect at Closing

Do you know what's on your credit report?

Learn what your score means.